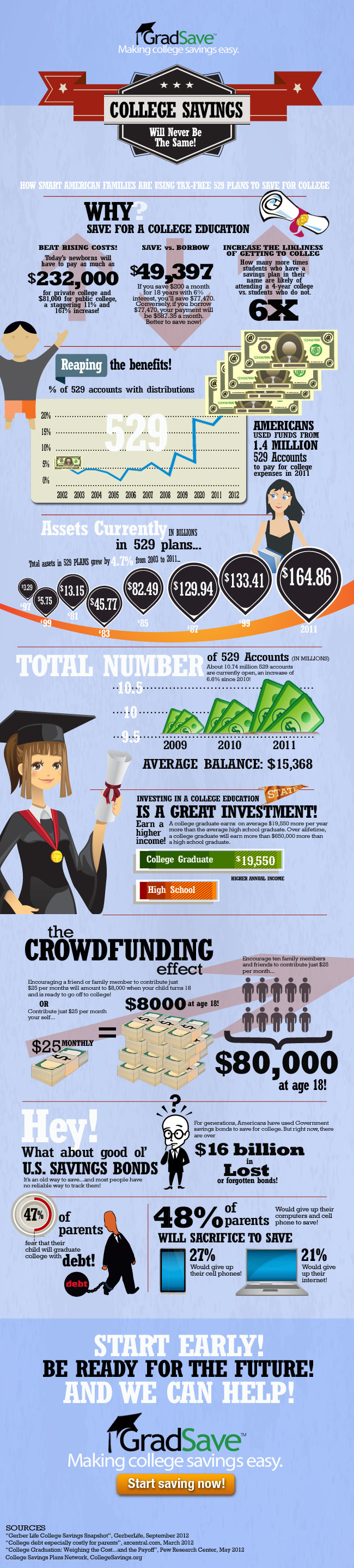

529 plans are tax advantaged asset vehicles in US and these are managed by the state or by an educational institution. These plans are specifically designed to assist and encourage families to set aside money for future college education expenses. 529 plans are named after the Internal Revenue Code’s section # 529. These plans were created in 1996.

There are 2 kinds of 529 plans and these include the savings and prepaid plans. Prepaid plans will let you pay the tuition fee at the recent cost and attend classes someday while the savings plans are investing in bond and stock funds. The major problem about the prepaid plans is that nobody knows the exact school where the students will take classes. Savings plans are relatively more flexible.

529 plans are very helpful but these can also trigger problems at some extent. The following are the pros and cons of 529 plans that you should know.

The Pros of 529 Plans

1. High Maximum Amount of Contribution

Unlike the other forms of education savings cars, 529 plans will usually let you make a higher or maximum yearly contribution. Every state is allowed to set its contribution limits and in certain states, the maximum is approximately $300,000 yearly.

2. Tax Advantages

The savings plans will offer some tax benefits to investors. 529 plans provide tax-deferred savings as well as tax-free distributions for eligible withdrawals. A certified withdrawal involves expenses associated to tuition, books, fees, equipment & in some instances, board and room expenditures are covered. Aside from that, there are some states where the investors are permitted to deduct partial or full contributions or get an income exception for withdrawals.

3. Availability

Investing in these plans isn’t limited to a particular form of investor. There is no age and income restriction associated with opening and availing these plans. In other cases, you could open a new account for only $25. You don’t need to reside inside a particular state so that you can take part in this program. Upon withdrawal, the funds could pay for eligible expenses at 2 or 4 year public/private institutions.

The Cons of 529 Plans

On the other hand, 529 plans are also associated with certain issues. These involve the following:

1. Restricted Investment Options

Depending on the plan you have availed, your investment choices with 529 plans might not be restricted compared to those that are provided by other savings vehicles. Usually, 529 plans provide mutual funds instead of individual bonds or stocks. You can’t transfer bonds and stocks that you already have with these plans without settling them first. Additionally, you can only alter your investment options once every year.

2. Probable Penalties

The main caveat of 529 plans is that you should use funds for the qualified education expenditures and you need to do it within a certain period of time. Withdrawals that are used for expenditures which are not actually related to education will be subject for a standard income tax & a ten percent withdrawal fee. You have to withdraw funds before your beneficiary reaches the age of 30 in order to prevent incurring a fifty percent tax fine.

How Do You Feel About 529 Plans?

529 plans are truly a great help for parents but since it is associated to some issues, many parents are discouraged to consider these plans for the sake of their child’s future. As a parent, what can you say about this?

{kind=link}